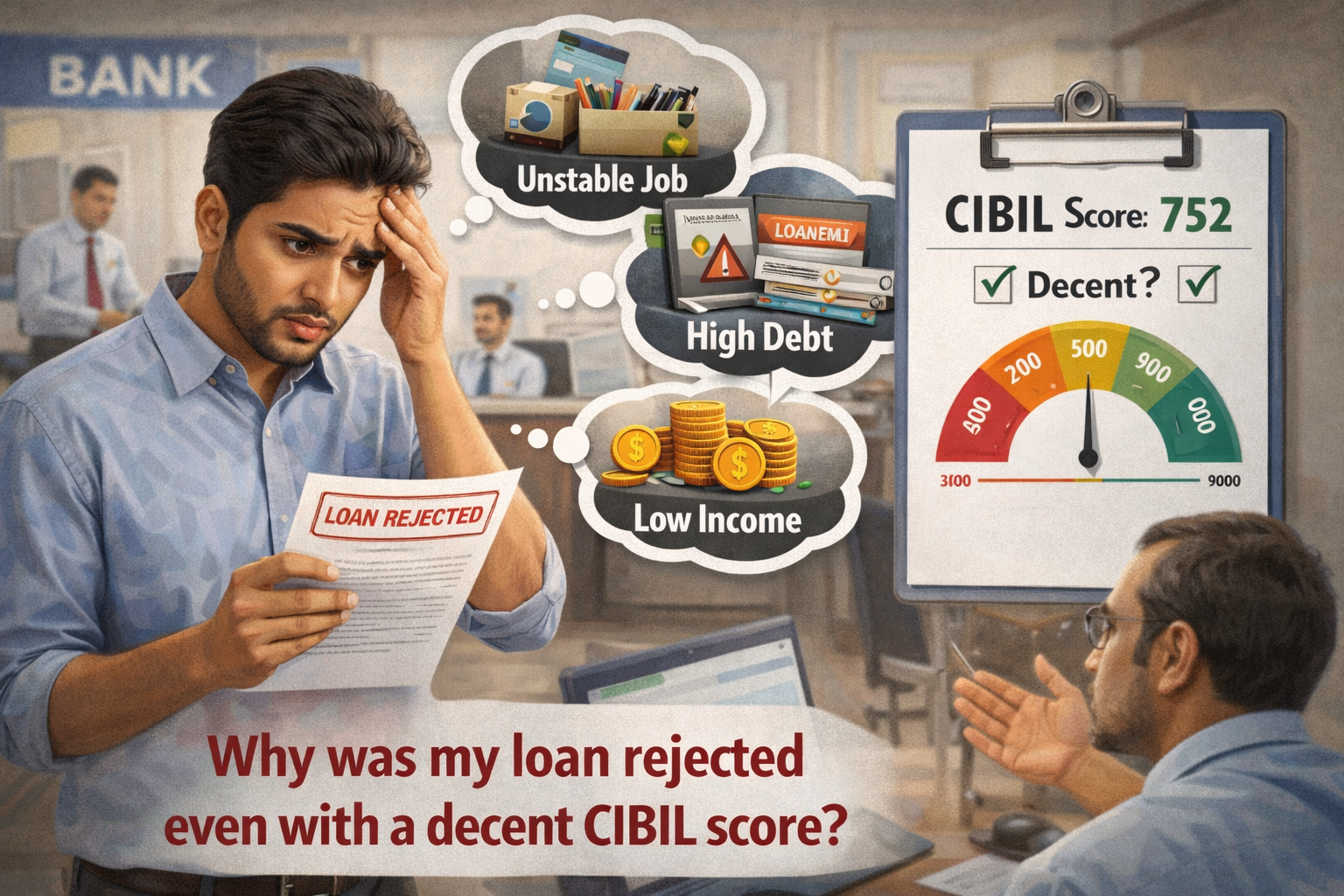

Kartik sat across from me last month, completely baffled. He’d just been rejected for a home loan—the third rejection in two months.

“My CIBIL score is 768,” he said, showing me his phone. “That’s good, right? So why does every bank keep saying no?”

I pulled up his bank statements and credit report. Within five minutes, I spotted at least six red flags that had nothing to do with his credit score.

Multiple job changes in 18 months. Bank account constantly hovering near zero. Four different loan inquiries in the past 60 days. Salary credits that didn’t match his stated income.

No wonder banks were rejecting him.

“But my score is good!” he protested.

That’s when I had to explain something most people don’t understand: your CIBIL score is just one piece of a much larger puzzle. And sometimes, it’s not even the most important piece.

I’ve spent over 12 years working with banks and watching loan applications get approved or rejected. Let me tell you exactly what’s happening behind the scenes—the stuff banks will never tell you in a rejection letter.

The Brutal Truth About CIBIL Scores

Here’s what banks tell you: “Maintain a good credit score and you’ll get loans easily.”

Here’s what they don’t tell you: a good score just gets your application past the first filter. The real evaluation happens after that.

Think of it like a job interview. A good resume gets you in the door. But it doesn’t guarantee you’ll get hired. The actual interview—where they dig into everything about you—that’s where decisions get made.

Your credit score is the resume. The bank loan approval process is the interview.

And just like job interviews, you can fail for reasons that have nothing to do with your qualifications on paper.

What “Decent” Actually Means (And Why It’s Not Enough)

Let me break down credit score ranges and what they really mean to banks:

300-549: Banks won’t even look at your application. You’re considered high-risk. Some NBFCs might give you loans but at terrible interest rates.

550-649: You’ll struggle. A few lenders might approve you for small amounts, but expect high interest rates and tough terms.

650-699: This is where it gets tricky. Banks call this “fair.” Some will approve you, some won’t. Your other factors become critical here.

700-749: Considered “good.” You’ll get approved more often than not—but only if everything else checks out. This is where most rejections happen despite decent scores.

750-899: “Excellent” range. Banks love you—but can still reject you for other reasons. I’ve seen plenty of rejections in this range.

900: Nearly impossible to achieve and maintain. If you have this, you’re either gaming the system or you’re the most financially disciplined person alive.

Most people think 700+ means automatic approval. It absolutely doesn’t.

I’ve seen someone with a 792 score get rejected while someone with a 682 score got approved for the same loan amount at the same bank. Why? Everything else on their application was different.

The Hidden Factors Banks Actually Look At

When you apply for a loan, banks run your application through multiple layers of scrutiny. Your CIBIL score is just layer one.

1. Your Income Stability (Not Just Income Amount)

Banks don’t just want to know you earn ₹80,000 a month. They want to know if you’ll still be earning it six months from now.

What they’re checking:

- How long you’ve been with your current employer

- Your employment gaps in the past 3 years

- Industry you work in (some are considered riskier)

- Job title and role stability

- Whether you’re on probation

I had a client earning ₹1.2 lakh monthly get rejected for a ₹15 lakh personal loan. Why? He’d changed jobs four times in two years. The bank saw him as unstable, regardless of his current income.

Another person earning just ₹55,000 but working at the same company for eight years? Approved without hesitation.

Job-hopping might boost your salary, but it destroys your loan eligibility. Banks hate uncertainty.

2. Your Debt-to-Income Ratio (The Silent Killer)

This is one of the biggest loan rejection reasons that nobody talks about.

Your debt-to-income ratio is: (Total Monthly EMIs ÷ Monthly Income) × 100

Banks have strict cutoffs:

- Below 40%: You’re in good shape

- 40-50%: Yellow flag—they’ll scrutinize everything else carefully

- Above 50%: Red flag—most banks auto-reject

- Above 60%: Almost guaranteed rejection

Here’s what most people miss: banks calculate this based on your gross income but look at your net obligations.

Let me show you a real example:

Meera earns ₹90,000 per month. She has:

- Home loan EMI: ₹28,000

- Car loan EMI: ₹12,000

- Credit card minimum payments: ₹8,000

Her ratio: (48,000 ÷ 90,000) × 100 = 53.3%

She applied for a personal loan with a ₹15,000 monthly EMI. The bank calculated her potential ratio as 64.4%. Instant rejection, despite her 745 CIBIL score.

The bank didn’t tell her this was the reason. They just said “application doesn’t meet our criteria.”

3. Your Banking Behavior (They’re Watching Everything)

If you’re applying for a loan from the bank where you have a salary account, they can see everything:

- Your average monthly balance over the past 6-12 months

- How many times you’ve hit minimum balance

- Bounced cheques or failed auto-debits

- Overdraft frequency

- Bill payment patterns

- Whether you’re constantly withdrawing your entire salary

I’ve seen applications rejected because the person’s bank account showed:

- Salary of ₹70,000 credited on the 1st

- Balance drops to ₹3,000 by the 5th

- Multiple ₹500-₹1,000 withdrawals throughout the month

- Regular minimum balance violations

This screams “poor money management” to banks. They think: if you can’t save anything from ₹70,000 monthly, how will you manage an additional ₹20,000 EMI?

4. Credit Inquiries (You’re Shooting Yourself in the Foot)

Every time you apply for a loan or credit card, the bank does a “hard inquiry” on your credit report. This gets recorded.

Too many inquiries in a short time is a massive red flag.

Why? Banks think you’re desperate for credit. Maybe you’re in financial trouble. Maybe you’re planning to take multiple loans and max out. Either way, it looks bad.

What’s “too many”?

- 1-2 inquiries in 3 months: Normal, no problem

- 3-4 inquiries: Yellow flag

- 5+ inquiries: Red flag, likely rejection

Kartik, the guy from my opening story? He had seven inquiries in 90 days. He’d applied at three different banks for a home loan, two banks for personal loans, and two credit card applications.

Each rejection made him panic and apply somewhere else. Each application made the next rejection more likely.

This is called “loan stacking behavior” and banks hate it.

5. Loan Type Mix (The Invisible Factor)

Banks prefer seeing a healthy mix of secured and unsecured loans in your credit history.

Secured loans: Home loan, car loan, loan against property (backed by collateral)

Unsecured loans: Personal loan, credit cards (no collateral)

If your credit report shows only personal loans and credit cards, banks see you as risky. Why don’t you have assets? Why is all your debt unsecured?

Conversely, if you have only secured loans and now apply for an unsecured one, banks wonder why the sudden change.

The ideal mix is about 60-70% secured and 30-40% unsecured. But this is one of those things banks never explicitly tell you.

6. Geographic and Demographic Profiling

This one makes people angry, but it’s real.

Banks have internal risk models based on:

- Your residential area (pincode-level risk assessment)

- Your workplace location

- Your native place

- Your type of residence (owned vs rented vs company accommodation)

Some pincodes are flagged as “high default zones” based on historical data. If you live there, you face extra scrutiny regardless of your personal credentials.

I’ve seen identical applications—same income, same credit score, same job—get different results based purely on pincode.

Is this fair? Probably not. But it’s how risk modeling works. Banks use statistical patterns, and sometimes you get caught in them unfairly.

Internal Bank Policies Nobody Explains

Every bank has internal lending policies that change based on their business needs. This is why timing matters more than people realize.

Monthly and Quarterly Targets

Banks have loan disbursement targets. Early in the month or quarter, they’re more lenient because they need to hit numbers. Toward the end, if they’ve already met targets, they get pickier.

I’ve literally seen the same application get rejected in week 1 and approved in week 4 of the month—at the same bank.

Portfolio Balancing

If a bank has too many personal loans on their books, they might start rejecting personal loan applications even from qualified candidates. They need to balance their loan portfolio across different products.

Similarly, if they’ve had high defaults in a particular industry (say, real estate or travel), they might start rejecting everyone from that sector for a few months.

You get caught in this, and you’ll never know that’s why you were rejected.

Risk Appetite Changes

During economic uncertainty, banks reduce their risk appetite across the board. Suddenly, the 710 CIBIL score that would’ve gotten you approved last month isn’t enough this month.

Post-COVID, I saw banks tighten their criteria significantly. People who would’ve sailed through in 2019 were getting rejected in 2020-21 with the same credentials.

Relationship Banking Weight

If you’ve been a customer at the bank for years, maintain healthy balances, and have never defaulted, you get preference. Banks call this “relationship value.”

Two people with identical applications—one is a 6-year customer, one is brand new—the existing customer has a significant advantage.

This is why people often get better loan terms from their salary account bank.

Common CIBIL Score Myths People Believe

Let me bust some myths that cost people approvals:

Myth 1: “A high CIBIL score guarantees loan approval”

Wrong. It increases your chances significantly, but it’s not a guarantee. I’ve seen 810+ scores get rejected for reasons I’ve explained above.

Myth 2: “Checking my own CIBIL score will lower it”

False. Checking your own score is a “soft inquiry” and doesn’t affect your score. Only when banks check it during loan applications (hard inquiry) does it have a minor impact.

Myth 3: “Closing old credit cards will improve my score”

Actually, it can hurt you. Credit history length matters. Closing your oldest card can reduce your average account age and lower your score.

Myth 4: “Zero debt means excellent creditworthiness”

Not exactly. Having no credit history makes banks nervous. They prefer seeing that you’ve successfully managed credit before. This is why some people with zero loans get rejected while people with well-managed existing loans get approved.

Myth 5: “Once rejected, I should immediately apply at another bank”

Terrible idea. Each application adds a hard inquiry. Multiple rejections in quick succession make you look desperate and hurt your chances further. Wait at least 3-6 months between applications.

Myth 6: “The bank will tell me exactly why I was rejected”

They won’t. You’ll get a generic “doesn’t meet our criteria” response. Banks rarely share specific internal reasons for rejection.

The Real Reasons Banks Reject Loans (That They Won’t Tell You)

Based on my experience reviewing hundreds of rejections, here are the actual reasons:

1. Inconsistent documentation: Your salary slips say ₹60,000 but bank statements show only ₹52,000 credits. Where’s the ₹8,000 difference? Is it going to another EMI you didn’t disclose?

2. Address mismatches: Your Aadhaar, PAN, salary slip, and current address are all different. Banks see this as instability or potential fraud.

3. Too many co-signed loans: You’re a guarantor on three other loans. If those people default, you’re liable. Banks factor this into your risk.

4. Negative public records: Court cases, bankruptcies, disputes—even if they’re civil matters unrelated to debt, they can affect approval.

5. Industry-specific concerns: You work in an industry facing headwinds. Even if your company is stable, banks might flag the entire sector.

6. Age and loan tenure mismatch: You’re 52 and applying for a 20-year home loan that goes till age 72. Most banks have maximum age limits at loan maturity.

7. Informal income sources: You earn ₹40,000 salary but show ₹80,000 in your application because you do freelancing. If you can’t document that freelance income properly with tax returns, banks won’t count it.

8. Social media and digital footprint: Some new-age lenders check social media and online behavior as part of their assessment. If your LinkedIn shows you job hunting actively, it raises flags.

What to Do When Your Loan Gets Rejected

Getting rejected feels terrible. But panicking and applying everywhere makes it worse.

Here’s what you should actually do:

Step 1: Get the Rejection in Writing

Call the bank and request a formal rejection letter or email. Some banks resist, but persist. You have a right to know the application status officially.

Step 2: Request Specific Reasons

Ask directly: “Can you tell me which parameters didn’t meet your criteria?”

They might not give detailed answers, but sometimes you’ll get hints:

- “Income level not sufficient” → Your debt-to-income ratio was too high

- “Employment criteria not met” → Job stability issues

- “Documentation incomplete” → Missing or inconsistent papers

- “Credit assessment” → Something on your credit report

Step 3: Get Your Credit Report

Don’t just check your CIBIL score. Get the full report from CIBIL, Experian, Equifax, and CRIF High Mark.

Look for:

- Errors or outdated information

- Accounts you don’t recognize

- Incorrect outstanding balances

- Settled accounts still showing as open

Errors are shockingly common. I’ve seen people get rejected because their credit report showed a ₹45,000 outstanding on a credit card they’d closed two years ago. One dispute letter fixed it.

Step 4: Don’t Apply Anywhere for 3-6 Months

I know it’s frustrating, but stop. Let the recent inquiries age off. Use this time to fix whatever went wrong.

If you desperately need the money, look at alternatives:

- Personal loan from your employer

- Gold loan (if you have jewelry)

- Loan against FD/insurance policy

- Borrowing from family

These don’t involve credit checks and won’t add more inquiries.

Step 5: Fix the Actual Problems

Based on what you find, take corrective action:

If it’s job stability: Stay at your current job for at least 12 months before reapplying. Banks want to see consistency.

If it’s debt-to-income ratio: Pay down existing loans. Even prepaying ₹50,000-₹1 lakh on a loan can make a difference.

If it’s bank account behavior: Start maintaining higher balances. Stop bouncing payments. Show 6 months of disciplined banking.

If it’s credit report errors: File disputes immediately. This can take 30-60 days to reflect.

If it’s too many credit cards: Close the newest ones, keep the oldest. Reduce your total available credit limit if it’s extremely high.

Step 6: Try a Different Loan Product

If you were rejected for a personal loan, you might get approved for a loan against FD or gold loan. Secured loans are easier to get because the bank has collateral.

Once you build a relationship with a secured loan and repay it well, unsecured loans become easier.

Step 7: Consider a Co-Applicant

Adding a co-applicant with strong credentials can dramatically improve approval chances:

- Working spouse

- Parent with good credit

- Sibling with stable job

Their income gets added, the debt-to-income ratio improves, and banks see reduced risk.

Just make sure the co-applicant actually has strong financials. Adding someone with their own credit problems makes it worse.

How to Improve Your Chances Before Applying

If you haven’t applied yet, here’s how to maximize approval probability:

3-6 Months Before:

- Check all your credit reports and fix errors

- Pay down existing loans where possible

- Stop applying for new credit completely

- Maintain high bank balances consistently

- Ensure zero bounced payments

1-3 Months Before:

- Gather all documentation (salary slips, bank statements, ITR, property papers)

- Ensure all documents have consistent information

- Pre-check your eligibility on the bank’s website

- Talk to a relationship manager if you’re an existing customer

Before Applying:

- Calculate your debt-to-income ratio yourself

- Make sure it’s below 45%

- Choose the right bank (the one where you have salary account usually gives best chances)

- Apply for a loan amount you can comfortably manage, not the maximum eligible

During Application:

- Disclose everything honestly (they’ll find out anyway)

- Don’t inflate your income

- Include all existing loans and credit cards

- Provide all documents in first attempt (incomplete applications often get rejected)

The Credit Score vs Loan Eligibility Reality

The relationship between credit score vs loan eligibility is more complex than a simple number.

Your credit score tells banks: “This person has managed credit responsibly in the past.”

But banks also want to know:

- Can they afford this new loan?

- Is their income stable?

- Are they in financial distress right now?

- Do they have good money management habits?

- Will they still be employed in 6 months?

A high score answers the first question. It doesn’t automatically answer the rest.

This is why understanding the full bank loan approval process matters more than obsessing over your score alone.

When to Give Up and When to Try Again

Sometimes, the answer is genuinely “not now.”

Don’t reapply if:

- You were rejected less than 3 months ago

- Your circumstances haven’t changed

- You’re just trying different banks with the same profile

- You’re already at 50%+ debt-to-income ratio

Do try again if:

- It’s been 6+ months since rejection

- You’ve fixed specific issues (paid down debt, changed jobs, fixed credit report errors)

- You’re applying at a different bank where you have an existing relationship

- Your income has increased significantly

- You’re applying with a strong co-applicant

Be patient. Building creditworthiness takes time, but it pays off with better loan terms and lower interest rates when you finally do get approved.

Frequently Asked Questions

Q1: Can I get a loan with a 680 CIBIL score?

Yes, but it depends on everything else in your profile. At 680, you’re in the borderline zone where other factors become critical. If you have stable employment, low debt-to-income ratio, and clean banking behavior, you can get approved. But expect slightly higher interest rates than someone with 750+. Some banks might reject you at 680 for unsecured loans but approve you for secured ones.

Q2: How long does a loan rejection stay on my credit report?

The rejection itself doesn’t appear on your credit report. What appears is the “hard inquiry” the bank made when you applied. This stays for 2 years but only impacts your score for about 6-12 months. The real damage is when you have multiple inquiries in a short period—that pattern is what hurts.

Q3: Should I take a loan from an NBFC if banks reject me?

NBFCs have more relaxed criteria than banks, so they might approve you when banks won’t. But they also charge higher interest rates—sometimes 3-5% more than banks. Use NBFCs only if: (a) you’ve been rejected by multiple banks, (b) you need the money urgently, and (c) you have a solid plan to repay quickly. Never take an NBFC loan for non-essentials.

Q4: Will getting a credit card help my loan application later?

Yes, if managed properly. A credit card builds your credit history. Use it for small purchases, pay the full amount on time every month, and keep utilization below 30% of the limit. After 12-18 months of this behavior, your credit profile strengthens significantly. But if you miss payments or max out the card, it destroys your chances.

Q5: Can I dispute a loan rejection?

You can’t “appeal” the decision like a legal case, but you can request reconsideration if you believe there was an error. Provide additional documentation, clarify discrepancies, or add a co-applicant. Some banks will review again, but most stick to their original decision. Better to fix issues and reapply after 6 months.

Q6: Do banks share rejection reasons with credit bureaus?

No. The credit bureau records that the bank made an inquiry, but not whether you were approved or rejected. However, if you’re rejected and don’t get a loan elsewhere, it’s obvious from your report that inquiries didn’t result in new accounts—which future lenders can see.

Q7: Is my CIBIL score different at different banks?

Your score is the same everywhere, but banks might use different credit bureaus (CIBIL, Experian, Equifax, CRIF). Your score can vary slightly across bureaus because they might have different information. Also, banks use their own internal scoring models on top of the bureau score, so their final risk assessment can differ.

Q8: Can I remove hard inquiries from my credit report?

Only if they were made without your permission (fraud). Legitimate inquiries from your own applications stay for 2 years. However, you can add a “consumer statement” to your credit report explaining a situation (like multiple inquiries were for a single loan, not multiple loans). Not all lenders read these, but some do.

The Bottom Line

Why was your loan rejected even with a decent CIBIL score?

Because banks evaluate at least 15-20 different factors, and your credit score is just one of them.

Your job stability, debt-to-income ratio, banking behavior, loan inquiry pattern, documentation consistency, employment sector, residential area, and even the bank’s current lending priorities all play a role.

Most rejections happen because of issues you can actually fix—you just didn’t know they mattered.

The good news? Now you know exactly what banks are looking for beyond just a number.

Fix the underlying problems. Give it time. Reapply strategically.

Your loan rejection today doesn’t have to be permanent. It’s often just a signal that you need to strengthen your financial profile before trying again.

And when you do get approved—and you will if you address these issues—you’ll likely get better terms too.

Financial Disclaimer: This article provides general information based on the author’s experience in banking and credit assessment in India. Loan approval criteria vary by lender and change over time. Individual circumstances differ significantly. This is not personalized financial or credit advice. Always verify current lending policies with specific lenders and consult a certified financial advisor for decisions specific to your situation.