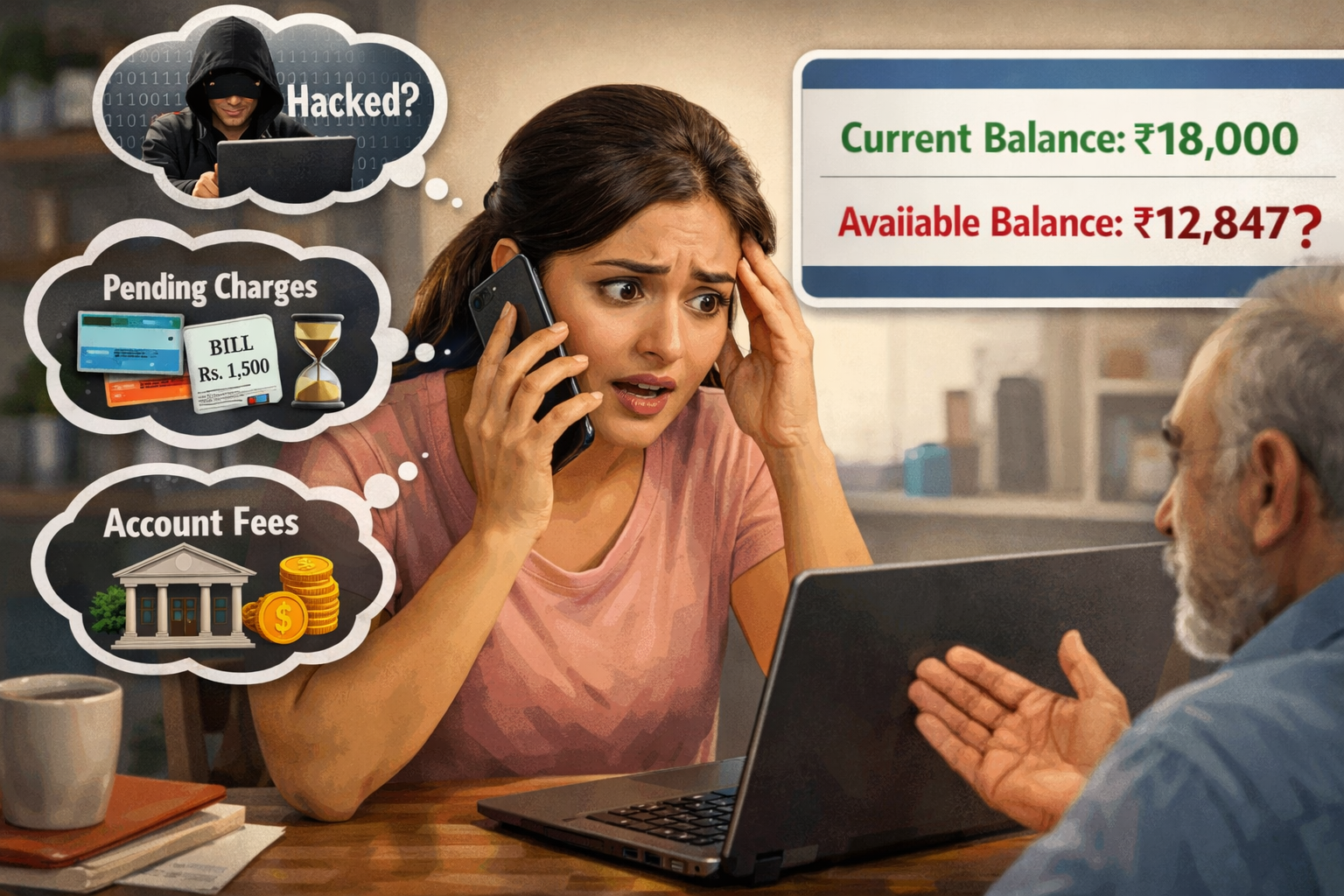

Last Tuesday, my neighbor Sarah called me in a panic. She’d just checked her bank account online and nearly dropped her phone. The balance showed ₹12,847 when she was certain she had around ₹18,000.

“Did someone hack my account?” she asked, her voice shaking.

I’ve heard this story at least a dozen times over my career in banking. And honestly? It’s rarely a hack. What most people don’t realize is that your “available balance” and what you think you have are often two very different numbers.

Let me walk you through exactly why this happens—and more importantly, what you can do about it.

The Two Balances Your Bank Hides in Plain Sight

Your bank account actually shows you multiple balances at once, and most people don’t know the difference.

Your “available balance” is what you can actually spend right now. Your “current balance” might be ₹5,000 higher because it includes money that’s technically there but frozen for various reasons.

Think of it like this: imagine someone hands you ₹5,000 in cash, but they say “don’t spend this until Friday.” You have the money, but you can’t use it yet. That’s basically what happens in your bank account constantly.

Here’s what trips people up: your banking app shows both numbers, but most folks only glance at one—usually the higher one—and make spending decisions based on that.

Wrong move.

The Most Common Culprits Behind Missing Money

1. Pending Transactions Are the Silent Balance Killers

When you swipe your debit card at a restaurant or shop, that money doesn’t disappear from your account instantly. The merchant sends a request to your bank, your bank “holds” that amount, but the actual transaction might not clear for 2-5 days.

During those days, your current balance still shows the money, but your available balance doesn’t.

I’ve seen people accidentally overdraft because they kept spending based on their current balance, not realizing they had ₹3,000 worth of pending UPI payments about to hit.

Here’s a real example from last month: A customer made three online purchases on Friday evening—₹2,400, ₹1,800, and ₹950. His app showed ₹8,200 current balance. He thought he was fine and spent another ₹4,500 over the weekend. Monday morning? Overdraft fees because all those Friday transactions processed simultaneously.

2. Cheques Take Forever (And People Forget About Them)

You write a cheque, give it to someone, and then completely forget about it.

That person might not deposit it for two weeks. Suddenly, when they do, boom—your balance drops unexpectedly.

The bank has no way of warning you because they don’t know about the cheque until someone presents it.

What most people don’t realize is that cheques can be valid for up to 3 months. So that payment you made in January could hit your account in March.

I once had a client who wrote six post-dated cheques for his kid’s tuition fees. He’d accounted for them mentally but never wrote them down. Five months later, all six cleared within two weeks of each other, and he couldn’t figure out where ₹72,000 went.

3. Auto-Debits and Standing Instructions You Forgot About

This one gets everyone eventually.

You signed up for Netflix last year. Or maybe that gym membership you used twice. Perhaps an insurance premium or SIP mutual fund investment.

These auto-debits sit quietly in the background, and then one day—usually when you’re running low on cash—they all decide to process at once.

I had a colleague who discovered she was paying for three streaming services she’d forgotten about, a gym she hadn’t visited in eight months, and a magazine subscription she didn’t even remember signing up for. Total damage? ₹2,100 per month for over a year.

Make a list of every single recurring payment. Review it every three months. You’d be surprised how many subscriptions you’re paying for that you don’t even use anymore.

4. Bank Holds on Large Deposits

You deposit a large cheque—let’s say ₹50,000. Your bank shows it in your balance, but they’ve put a “hold” on it for 3-7 days.

Why? Because they want to make sure the cheque actually clears from the other person’s bank first.

During this holding period, the money shows up in your current balance but not your available balance. Try to withdraw it and you’ll get an “insufficient funds” message even though you can clearly see the money there.

This is especially common with:

- Cheques from other banks

- Large cash deposits at ATMs

- International transfers

- First-time deposits from new sources

The frustrating part? Different banks have different hold policies. Some release funds in 24 hours for good customers. Others take the full week regardless of your relationship with them.

5. Hidden Bank Fees and Charges

Banks have gotten creative with fees, and not in a good way.

Some charges that might silently eat into your balance:

- Minimum balance penalties (usually ₹500-₹750 per month)

- SMS alert charges (₹15-₹25 per month)

- Debit card annual fees (₹150-₹500)

- ATM withdrawal charges after your free limit (₹20 per transaction)

- Cheque book issuance fees (₹75-₹200)

- NEFT/RTGS charges below certain amounts

- Account maintenance charges (quarterly)

These typically get deducted quarterly or annually, so people forget they exist.

In my banking days, I saw customers lose ₹2,000-₹3,000 per year just in fees they didn’t know they were paying. One person was getting charged ₹600 every quarter for “non-maintenance of minimum balance” because he kept his account at ₹9,800 when the requirement was ₹10,000.

The Technical Stuff Banks Don’t Explain Well

Authorization Holds Are Sneaky

Ever noticed hotels and petrol pumps block more money than you actually spend?

Here’s how it works: You check into a hotel with a ₹5,000 room charge. The hotel puts an authorization hold of ₹8,000 on your card “just in case” you raid the minibar or make phone calls.

You check out, pay ₹5,000, but that extra ₹3,000 stays blocked for another 3-7 days.

Same thing happens at fuel stations. They authorize ₹2,000, you fill ₹1,200 worth of petrol, but the full ₹2,000 gets held until the transaction settles.

Rental cars are the worst offenders. They’ll hold ₹15,000-₹20,000 as a deposit, and even after you return the car, that money stays frozen for up to 10 days.

Weekend and Holiday Delays

Banking doesn’t really happen on weekends or bank holidays.

If you make a transaction Friday evening, it probably won’t process until Monday. If Monday is a holiday, maybe Tuesday.

But your available balance drops immediately because the bank knows the money is “spoken for.”

This creates a weird gap where money leaves your available balance but hasn’t actually left your account yet.

I’ve seen this cause major problems during festival seasons when there are multiple bank holidays clustered together. Transactions pile up, and when everything processes at once, balances drop sharply.

What to Do When Your Balance Doesn’t Make Sense

Step 1: Don’t Panic

I know it’s scary to see less money than expected. But in 95% of cases, there’s a boring explanation.

Take a breath. Don’t assume fraud right away.

Step 2: Check Your Transaction History Carefully

Log into your banking app and look at the last 7-10 days of transactions.

Look for:

- Transactions you forgot about

- Duplicate charges (these happen more than you’d think)

- Merchant names you don’t recognize (sometimes they process under parent company names)

I once spent 20 minutes helping someone figure out that “AMZN MKTP” was just Amazon Marketplace. They’d ordered something weeks ago and completely forgotten.

Other confusing merchant names I’ve seen: “SQ *COFFEE SHOP” (Square payment processor), “PAYPAL *MERCHANT” (any PayPal transaction), “GOOGLE *TEMPORARY HOLD” (Google Pay authorization).

Step 3: Separate Current Balance from Available Balance

Most banking apps show both numbers, but people only look at one.

Your current balance is always higher because it includes pending deposits and hasn’t subtracted pending debits yet.

Always make spending decisions based on your available balance, not your current balance.

Step 4: Review Pending Transactions

Every banking app has a “pending transactions” section, though some banks hide it in the menu.

Check it religiously.

These are transactions that have been authorized but not yet cleared. They’re already reducing your available balance even though they don’t show up in your transaction history yet.

Step 5: Contact Your Bank If Something Truly Doesn’t Add Up

If you’ve done all this and the math still doesn’t work, call your bank.

Ask them to explain every single deduction. They can see things on their end that don’t always show up in your app immediately.

Get a reference number for your call. If there’s an actual error, you’ll need it to file a dispute.

Common Myths People Believe About Bank Balances

Myth 1: “My balance updates in real-time”

Not even close. Most transactions take 24-72 hours to fully process. Your banking app is showing you an approximation, not exact real-time data.

Myth 2: “If I can see the money, I can spend it”

Nope. Just because money appears in your current balance doesn’t mean it’s available for withdrawal. Always check your available balance.

Myth 3: “Pending transactions will cancel if the merchant doesn’t charge me”

They’ll cancel eventually, but it can take 7-10 days. The hold stays until the authorization expires or the merchant processes the actual charge.

Myth 4: “My salary is available the moment it’s credited”

Most employers do salary transfers that process overnight. If your company initiates it on the 30th evening, you might not see it until the 1st morning—or even the 2nd if there’s a weekend involved.

Myth 5: “UPI transactions are instant, so they can’t be pending”

UPI debits your account instantly, but the merchant might not receive the money for 24-48 hours due to settlement cycles. During this time, your money is in a kind of digital limbo.

How to Prevent Balance Surprises

Keep a Manual Transaction Log

I know this sounds old-fashioned, but it works.

Use a simple notes app on your phone. Every time you spend money, jot it down immediately.

Compare this against your bank statement weekly.

You’ll catch discrepancies faster and you’ll have a much better sense of where your money actually goes.

I’ve been doing this for 8 years. Takes me maybe 30 seconds per transaction. Saves me hours of confusion every month.

Set Up Balance Alerts

Most banks let you set up SMS or email alerts for:

- Transactions above a certain amount (I set mine at ₹500)

- When your balance drops below a threshold (mine’s ₹15,000)

- Every single debit/credit (can be annoying but useful)

Set these up. They’re free and they’ve saved countless people from overdrafts.

Review Your Account Every Week

Pick a day—maybe Sunday morning—and spend 10 minutes reviewing your bank account.

Look for anything unusual. Check pending transactions. Make sure everything adds up.

This habit alone will prevent 90% of balance-related surprises.

Maintain a Buffer Amount

Never let your account run down to zero.

Keep at least ₹5,000-₹10,000 as a buffer. This protects you from:

- Forgotten auto-debits

- Bank fees

- Delayed transactions hitting when you least expect them

Think of it as your account’s emergency cushion. Not emergency fund—that’s separate—but just a cushion so you don’t accidentally bounce a payment.

The Connection to Loan Rejections (That Nobody Talks About)

Here’s where this gets interesting.

You know how people get confused about why their bank loan got rejected even though they have a decent CIBIL score?

Same kind of misunderstanding.

Banks look at way more than just your CIBIL score when deciding on loan approval. They look at your banking behavior. How you manage your account balance. Whether you’re constantly running on empty. Whether you have lots of bounced transactions.

I’ve reviewed loan applications where the person had a 780 credit score—excellent range—but their bank account told a different story:

- Regular minimum balance violations every month

- Three bounced cheques in the past year

- Constant overdrafts, even small ones

- No savings pattern whatsoever

- Account frequently dipping below ₹500

Banks see these as red flags. They think: “This person can’t manage the money they already have. Why would we lend them more?”

The loan rejection reasons banks don’t tell you often come down to these hidden patterns in your banking behavior, not just your credit score.

Understanding the Bank Loan Approval Process

Since we’re talking about bank balances and money management, let me share something most people don’t know.

The bank loan approval process isn’t just about meeting minimum criteria. Banks have internal policies that regular customers never see.

For example:

- Some banks won’t approve loans if you’ve changed jobs in the last 6 months (even if you didn’t mention it, they can tell from your salary credits)

- Others auto-reject if your EMI-to-income ratio crosses 50%, regardless of your credit score

- Many have minimum income requirements that vary by city—₹40,000/month in Mumbai might be fine, but ₹50,000 required in Delhi

- Some flag you if too many banks have checked your credit report in the last 3 months

These are the hidden reasons banks reject loans that they’ll never put in the rejection letter. They’ll just say “application not approved as per internal policy.”

One of the biggest CIBIL score myths is that a score above 750 guarantees approval. It doesn’t.

I’ve seen people with 800+ scores get rejected because:

- They had too many unsecured loans (personal loans, credit cards)

- Their income documentation wasn’t convincing (salary slips looked inconsistent)

- They lived in an area the bank considered “risky” based on default rates

- They had changed addresses too frequently (banks see this as instability)

- Their existing debt payments were too high

The relationship between credit score vs loan eligibility is important, but it’s not everything. Your credit score gets you in the door. Your banking behavior determines whether you walk out with approval.

Your Step-by-Step Action Plan

Immediate Actions (Do This Today):

- Download your bank statement for the last 30 days

- List every single pending transaction you can find

- Check for any unknown auto-debits in your transaction history

- Set up balance alerts if you haven’t already

- Write down all your recurring payments—streaming services, insurance, SIPs, everything

This Week:

- Review your minimum balance requirements (call your bank if you’re not sure)

- Calculate your average monthly spending from the last 3 months

- Set up a budget buffer of at least ₹5,000

- Enable transaction notifications for all amounts above ₹500

- Check if you have any old cheques outstanding that haven’t cleared

This Month:

- Cancel subscriptions you don’t use (be ruthless about this)

- Review all bank charges on your statement—question anything you don’t understand

- Consider consolidating accounts if you have too many (multiple accounts mean multiple minimum balances to maintain)

- Set up a simple tracking system for expenses (even a Google Sheet works)

- Check your CIBIL score (free once per year at official CIBIL website)

Ongoing Habits:

- Review your account every Sunday morning (10 minutes max)

- Reconcile your manual log with bank statements weekly

- Monitor pending transactions before making large purchases

- Keep your buffer amount topped up—treat it as untouchable

- Document any unexplained discrepancies immediately and follow up

Frequently Asked Questions

Q1: Why does my ATM balance show different from my app balance?

ATMs often show your current balance, which includes pending transactions. Your app usually shows available balance, which is more accurate for spending decisions. The ATM also might not update as frequently—sometimes the data is 24 hours old, especially at non-bank ATMs.

Q2: Can pending transactions cause me to overdraft?

Absolutely. If you keep spending based on what you see available without accounting for pending transactions, you can easily overdraft. The bank will still process those pending transactions even if your balance is now zero. And then you’ll get hit with overdraft fees on top of it.

Q3: How long do pending transactions stay pending?

Most debit card transactions clear within 2-5 business days. UPI is usually 24-48 hours. Cheques can take 3-7 days depending on the issuing bank. Authorization holds from hotels or car rentals might stay for 7-10 days. International transactions can take even longer.

Q4: Will the bank notify me before charging fees?

Usually no. Most maintenance fees, minimum balance penalties, and service charges happen automatically. You’ll only know when you see them on your statement. This is why reviewing your account regularly is so important. Some banks will send you a warning SMS if you’re about to incur a minimum balance penalty, but don’t count on it.

Q5: Can a merchant charge me twice by accident?

Yes, it happens more often than you’d think. Technical glitches, system errors, or human mistakes can cause duplicate charges. If you notice this, contact both the merchant and your bank immediately. Most banks can reverse duplicate transactions once verified, but you need to catch it within 60-90 days.

Q6: Why did my salary take longer to credit this month?

Bank holidays, weekends, and the timing of your employer’s payment run all affect this. If your salary usually comes on the 30th but that falls on a Sunday, it might not process until Monday or Tuesday. Some companies also delay salary processing if there are payroll issues or if it’s end of financial year.

Q7: Do banks purposely delay showing transactions to earn interest on my money?

This conspiracy theory comes up a lot, but no. The delays are mostly due to the interbank settlement process and how payment networks work. Banks do benefit from “float,” but the delays are largely systemic, not intentional manipulation. That said, some banks are faster at updating than others.

Q8: Can I spend money that shows in my current balance but not available balance?

No. If you try, the transaction will be declined or you’ll overdraft. Always go by your available balance for spending decisions. The current balance is just informational—it’s not actually available to you yet.

The Bottom Line

Your bank balance showing less than expected is usually not a crisis—it’s a communication gap between how banks process money and how we think they should.

Banks process transactions in ways that aren’t immediately obvious to regular customers. Pending transactions, authorization holds, forgotten auto-debits, and processing delays create confusion constantly.

The solution isn’t to stress every time your balance looks off. It’s to develop better habits around monitoring and understanding your account.

The people who never had “balance surprises” all did the same thing: they tracked their spending actively, checked their accounts regularly, and maintained a buffer.

It’s not complicated. It just requires consistency.

And here’s the bonus: when you manage your bank balance well, you’re also building the kind of financial behavior that makes banks trust you when you eventually need a loan, a credit card limit increase, or better interest rates.

Your banking habits tell a story about you. Make sure it’s a good one.

Financial Disclaimer: This article provides general information based on common banking practices and the author’s professional experience in the Indian banking sector. Banking policies, fee structures, and processing times vary by bank and region. Always verify specific details with your bank directly. This content is not personalized financial advice. For specific concerns about your account or transactions, contact your bank’s customer service or visit a branch.